Hero is being developed at a propitious moment, as the following demographic and economic factors show:

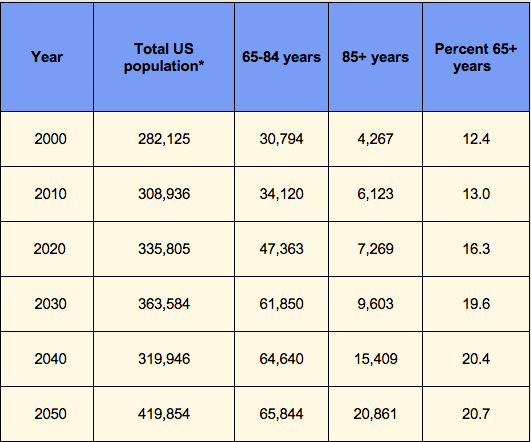

- Americans are aging. Over the six decades from 2000 to 2050, the total number of adults over 65 years will increase to 87 million from 35 million, to 21 percent from 12 percent of the nation’s population.

- Over four-fifths (81 percent) of all Americans 65 years and older are homeowners. (The New York Times estimates that they have $2 trillion in housing wealth)

- Home equity is often the largest part of the total assets of aging Americans.

- A large percentage of aging Americans are financially unprepared for retirement.

- The historic appreciation in real estate in recent years has changed public attitudes to this part of the investment world, encouraging a number of innovations, a change that augurs well for HERO.

- In recent years the number of reverse mortgages has grown dramatically. As of June 2006, more than 218,000 of such mortgages had been originated. The success of this type of loan, which enables the aging homeowner to convert home equity to cash, is a demonstration of the factors mentioned above and an indication of the size of the potential market for a program like HERO.

Aging of the Homeowner Population

The U.S. Census Bureau forecasts that the population will increase by nearly 50 percent by 2050, growing to 420 million. However, the total number of people 65 years and older will more than double, from 35 million to 87 million, and the relative proportion of seniors will increase from 12 percent in 2000 to 21 percent of the total population.

Table 1: U.S Projected Population, 2000 to 2005

* in millions

* in millions

Source: US Census Bureau, 2004, “U.S. Interim Projections by Age, Sex, Race and Hispanic Origin.”

According to U.S. Census data, seniors are overwhelmingly homeowners.

Table 2: Homeownership Rates by Age of Householder

Source: U.S. Census Bureau, Housing Vacancies and Homeownership, 2007

As indicated in Table 3, McKinsey & Co. recently reported on the median net worth of each age cohort.

Table 3: Median Net Household Worth, By Age Group

* in thousands

* in thousands

Source: McKinsey & Co., “Checking the Consumer Retirement Code,” p. 26.